Cotton growers intend to reduce plantings in difficult year ahead

February 09, 2015 |12:47 PM

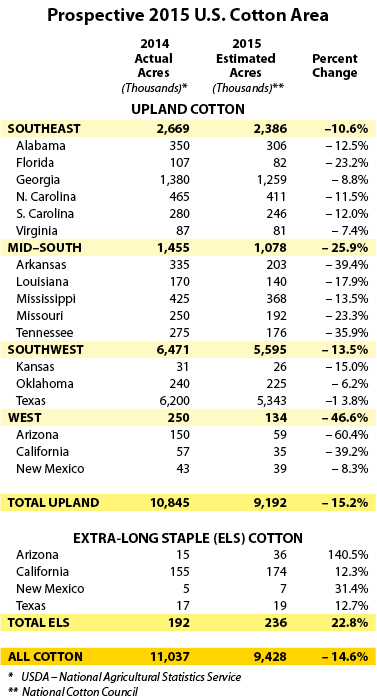

U.S. cotton producers intend to plant 9.4 million acres of cotton this spring, down 14.6 percent from 2014, as they face global cotton stocks at very high levels and uncertainties regarding global mill cotton use, the National Cotton Council said in a news release.

The NCC's 32nd annual Early Season Planting Intentions Survey showed:

Upland cotton intentions are 9.2 million acres, down 15.2 percent from 2014

Extra-long staple (ELS) intentions of 236,000 acres represent a 22.8 percent increase.

The survey results were announced at the NCC’s 2015 annual neeting in Memphis.

The NCC questionnaire, mailed in mid-December 2014 to producers across the 17-state Cotton Belt, asked for the number of acres devoted to cotton and other crops in 2014 and the acres planned for the coming season. Survey responses were collected through mid-January.

“History has shown that U.S. farmers respond to relative prices when making planting decisions,” noted Gary Adams, the NCC vice president for economics and policy analysis who became the president and CEO of the organization at the close of the meeting.

“Cotton growers are approaching the 2015 planting season with harvest-time futures contracts at the lowest level since planting of the 2009 crop,” Adams said. “After more than five years of stronger markets, cotton prices fell sharply during the second half of 2014.”

Southeast

Survey respondents throughout the Southeast indicated a 10.6 percent decline, lowering the regional total to 2.39 million acres. Declines are expected in each of the region’s six states as cotton acres move into competing crops.

Even with the expected reduction, the Southeast’s cotton acreage remains well above the recent low of 1.89 million acres in 2009.

In Alabama, the survey responses indicate a shift to peanuts and soybeans, while Florida’s acreage is almost exclusively moving to peanuts.

In Georgia, the acreage shifts are more varied with peanuts, corn and soybeans all expected to pull acres from cotton with South Carolina looking at a similar scenario.

In North Carolina, the shift is to soybeans, while corn benefits from the modest decline in Virginia.

Mid-South

In the Mid-South, survey results show that growers intend to plant 1.08 million acres, a decrease of 25.9 percent.

As was the case in the Southeast, all Mid-South states responded with intentions to plant less cotton in 2015. Without exception across the five states, the respondents indicate that cotton acres will move into soybeans for 2015.

Southwest

Southwest growers indicated a 13.5 percent decline, bringing the regional total to 5.60 million acres.

In Kansas, land shifting out of cotton is moving into corn and grain sorghum. Wheat is the expected beneficiary based on the Oklahoma survey results.

In south Texas, respondents indicate a shift out of cotton and into grain sorghum. Respondents from Texas’ Blacklands region are moving predominantly to wheat, with a smaller shift to corn. In West Texas, the acres shifting away from cotton are split between wheat, corn and grain sorghum.

West

The West accounts for the largest percentage reduction across the four production regions.

With upland intentions of 134,000 acres, those producers are expecting to plant 46.6 percent fewer acres of upland cotton. The 2015 acreage represents a new low for recent history.

The survey results for Arizona suggest a shift from cotton to wheat, as well as the “other crops” category. Upland growers also indicate a shift to ELS cotton.

In New Mexico, the cotton reduction coincides with responses indicating more acres of grain crops.

Survey results indicate U.S. cotton growers intend to increase ELS plantings 22.8 percent to 236,000 acres in 2015. If realized, that total would exceed the five-year average by 18,000 acres.

Extra-long staple cotton

ELS results reflect both the fact that ELS prices remain more attractive relative to upland cotton and likely capture expectations during the survey period of improved 2015 water availability in California. Final acreage will be affected by actual water allocations, which remain uncertain.

NCC delegates were reminded that these expectations are a snapshot of intentions based on market conditions at survey time. Actual plantings will be influenced by changing market conditions and weather.

“While world mill use in 2015 is expected to exceed world production in 2015, the differential does little to reduce global cotton stocks," Adams added.

Regarding domestic cotton mill use, Adams sees ongoing growth in U.S. textile industry consumption in 2015 with the Economic Adjustment Assistance Program continuing to spur investment in U.S. mills.

He projected a 100,000-plus bale increase in U.S. mill cotton use bringing total use to 3.7 million bales in 2015.

Exports continue as the primary outlet for U.S. raw fiber, Adams said. China is still the leading customer, even though that country’s imports have declined over the past year.

Adams said China has amassed more than 50 million bales in its government reserves, thus leading to less need to import cotton from the world market.

For 2015, China’s imports are projected at 6.2 million bales, down from 7.1 million in 2014 and well below levels observed in 2011 through 2013.

China’s mill use, though, is only seen realizing modest growth in 2015, Adams noted.

He said that China’s cotton price is almost twice the price of polyester – “a relationship that is not allowing cotton mill use in China to recover.”

India is projected to continue as the world’s largest cotton producer and seen exporting 5.9 million bales in 2015.

Adams said, though, “The potential for greater exports exists if the (Indian) government chooses to be more aggressive in the pricing of cotton from reserves.”